A senior enterprise solution architect with 19 years of banking-technology leadership across the Gulf, South Asia, and Africa was approved for an EB-2 NIW to advance AI-powered, quantum-resilient, vendor-neutral digital banking infrastructure for U.S. community banks and credit unions.

| Case Snapshot | Approved EB-2 NIW self-petition |

| Professional Profile | Enterprise solution architect with MCIT, MBA in Finance, BS in Computer Science, CISSP, TOGAF, AWS, Azure, and SAS GRC credentials. |

| Experience | 19 years designing and implementing mission-critical banking technology across more than 20 countries. |

| Proposed Endeavor | Design and implement a national financial-continuity and cybersecurity architecture for U.S. community banks and credit unions. |

| Core Technical Areas | AI fraud intelligence, federated learning, telecom-resilient banking infrastructure, zero-trust security, post-quantum cryptography, hybrid-cloud RegTech architecture. |

| Funding / Execution | Self-funded pilot model with personal seed capital and a phased plan to support community financial institutions. |

| Outcome | Approved under Matter of Dhanasar. |

Privacy note: The petitioner’s name, employer names, university names, referee names, collaborator names, and personal contact details have been withheld. The professional facts, proposed endeavor, and approval outcome are presented in anonymized form.

4,600 Banks, Rising Cybercrime, and a Technology Gap That Cannot Be Ignored

The approval centered on a clear national problem: many U.S. community banks and credit unions remain essential to small businesses, rural communities, agricultural lending, and local credit access, but they often lack the technology resources available to the largest national banks. EB-2 NIW

The petition framed this gap through cybersecurity, continuity, and modernization. EB-2 NIW The FBI reported $16.6 billion in cybercrime losses in 2024. Community financial institutions also face rising pressure from fraud, vendor concentration, legacy core systems, cybersecurity talent shortages, and the cost of adopting modern cloud, data, and compliance tools.

For USCIS, the case was not presented as a generic information-technology petition. It was built as a financial-continuity and infrastructure-modernization endeavor aimed at a specific underserved segment of the U.S. banking system. EB-2 NIW

The Career Behind the Approval

The petitioner began his banking-technology career in 2006 at one of South Asia’s largest banking institutions. Over the next 19 years, he moved from application and solution management into enterprise architecture, disaster recovery, digital banking platforms, compliance technology, and security-led modernization across more than 20 countries. EB-2 NIW

His work included branch automation consolidation, server centralization, high-availability architecture, international telecom redundancy, regional fintech and payment systems, SAP Hybris digital platforms, data-lake architecture for fraud monitoring and compliance reporting, and Customer 360-degree platforms connecting banking operations across multiple jurisdictions. EB-2 NIW

The profile was strengthened by formal credentials that directly matched the proposed endeavor. CISSP supported the cybersecurity component. TOGAF supported the enterprise-architecture component. AWS and Azure certifications supported the cloud-infrastructure component. SAS GRC supported the governance, risk, and compliance component. Together, these credentials showed that the proposed work was grounded in documented expertise, not general career aspiration. EB-2 NIW

The Proposed Endeavor: A Four-Part Architecture for Community Bank Resilience

The approved endeavor was structured around four integrated components. Each component addressed a defined weakness in the U.S. community banking environment and connected the petitioner’s prior experience to a practical U.S. implementation path.

1. AI-Powered Fraud Intelligence and Financial Continuity

The first component uses behavioral analytics, graph-based anomaly detection, explainable AI, and federated learning to detect fraud patterns without requiring institutions to share raw customer data. The petition emphasized a practical benefit for smaller banks: they could participate in shared fraud intelligence while keeping customer records within their own systems.

2. Telecom-Integrated Resilient Infrastructure

The second component addresses a weakness often overlooked in banking continuity planning: the network itself. The proposed model integrates multi-carrier failover, satellite backup, encrypted 5G pathways, SD-WAN, and AI-guided traffic routing so that banking services can continue during storms, carrier outages, cyberattacks, or local infrastructure failures.

3. Zero-Trust Security and Post-Quantum Cryptography

The third component moves smaller institutions away from perimeter-based security and toward continuous verification of users, devices, workloads, and application traffic. It also anticipates the transition to post-quantum cryptography, including NIST-standardized algorithms that are intended to protect sensitive information against future quantum-computing threats.

4. Hybrid-Cloud, Vendor-Neutral RegTech Architecture

The fourth component creates the foundation layer: standardized APIs, containerized microservices, vendor-neutral architecture, and embedded RegTech automation for AML, KYC, reporting, and supervisory compliance. The goal is to let community banks connect modern fintech tools without replacing their entire core banking system or becoming locked into one vendor ecosystem.

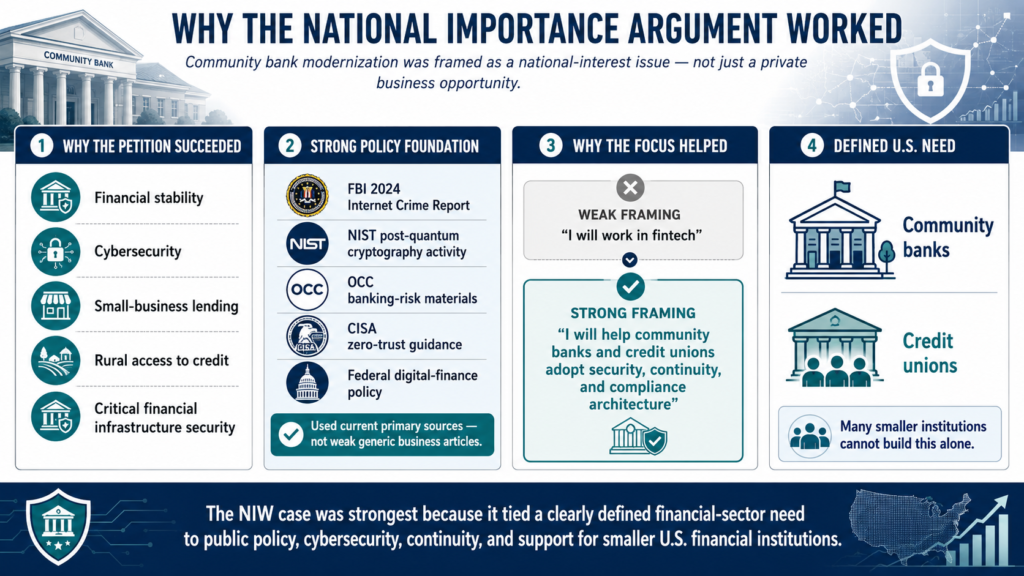

Why the National Importance Argument Worked

The petition succeeded because it did not describe community bank modernization as a private business opportunity only. It connected the endeavor to financial stability, cybersecurity, small-business lending, rural access to credit, and the security of critical financial infrastructure.

The national-importance section used current, primary sources: the FBI’s 2024 Internet Crime Report, NIST’s post-quantum cryptography standardization activity, OCC banking-risk materials, CISA zero-trust guidance, and federal digital-finance policy. This gave the petition a strong public-policy foundation and avoided reliance on weak or generic business articles.

The petitioner’s work was also tied to a specific population: community banks and credit unions. That focus helped avoid a common NIW weakness. The case was not framed as “I will work in fintech.” It was framed as “I will help a defined segment of the U.S. financial system adopt security, continuity, and compliance architecture that many smaller institutions cannot build alone.”

How the Dhanasar Prongs Were Presented

Prong One: Substantial Merit and National Importance

The petition presented substantial merit through the technical value of fraud detection, resilient network architecture, post-quantum security, and compliance automation. It presented national importance through documented risks to the U.S. financial sector, the role of community banks in local credit access, the scale of reported cybercrime losses, and federal recognition of cybersecurity and digital-finance modernization as ongoing policy concerns.

Prong Two: Well-Positioned to Advance the Endeavor

The well-positioned argument was one of the strongest parts of the case. The petitioner had already built banking infrastructure across multiple countries, held globally recognized architecture and cybersecurity certifications, managed enterprise modernization projects, and delivered systems in regulated financial environments. USCIS was given concrete evidence of progression, technical responsibility, and direct subject-matter fit.

Prong Three: Benefit of Waiving the Job Offer and Labor Certification Requirement

The waiver argument focused on scope and independence. The proposed work was not limited to one bank or one employer. It required an independent architecture model that could serve multiple community financial institutions, coordinate with vendors, integrate across platforms, and adapt to different regulatory and operational environments. The petition argued that requiring a single permanent job offer would narrow the very work that created the national-interest value.

The Outcome

Approved.

USCIS approved the EB-2 National Interest Waiver self-petition for a senior enterprise solution architect whose career in global banking technology, cybersecurity, cloud architecture, disaster recovery, and compliance automation was directly aligned with the proposed U.S. endeavor.

The approval confirms that financial technology cases can succeed under the NIW framework when they are presented as infrastructure-level contributions with national relevance, not as ordinary IT employment or private consulting. This case was approved because the proposed work addressed a documented public problem and the petitioner had a credible record of building the type of systems the endeavor required.

What Makes This Success Story Different

This case is distinct from general fintech, software, or cybersecurity stories because its target population was narrow and nationally important: U.S. community banks and credit unions. The petitioner was not proposing a general app, a single-company cybersecurity service, or an employment-based role. He proposed a vendor-neutral architecture for institutions that support local credit access but often lack the scale to modernize independently.

The technical combination also made the case stand out: federated fraud intelligence, telecom-integrated continuity, zero-trust security, post-quantum cryptography, hybrid-cloud architecture, and RegTech automation. These components formed a coherent national infrastructure proposal rather than a list of unrelated technology trends.

Questions Financial Technology and Enterprise Architecture Professionals Ask Us

Can a banking technology architect qualify for an EB-2 NIW?

Yes, when the proposed work is framed beyond ordinary employment. A banking technology architect can qualify where the endeavor addresses a nationally important financial-system problem and the petitioner has a documented record of building comparable systems. In this case, the national-interest argument focused on community bank modernization, cybersecurity resilience, fraud detection, continuity, and compliance architecture.

Does cybersecurity alone make a case nationally important?

Cybersecurity is important, but the petition still needs a specific national-impact theory. This case connected cybersecurity to the banking system, community financial institutions, fraud losses, operational continuity, regulatory compliance, and rural and small-business access to banking services. That made the national importance argument more concrete.

Why did post-quantum cryptography help the case?

Post-quantum cryptography helped because it showed that the petitioner was not only solving today’s banking-security problems. He was also addressing future risks to encrypted financial data. The petition connected this technical issue to NIST’s national standardization work, which gave the claim a credible federal-policy foundation.

Can international banking experience transfer to the U.S. financial sector?

Yes, if the petition explains the transfer clearly. Enterprise architecture, disaster recovery, cloud security, fraud analytics, and compliance automation are globally relevant disciplines. The petition showed that the petitioner had worked in regulated banking environments across multiple countries and that his technical methods could be adapted to U.S. community banking needs.

For Financial Technology, Cybersecurity, and Enterprise Architecture Professionals

This approval shows that a technology professional can build a strong EB-2 NIW case when the proposed work is tied to a defined national problem, supported by policy and industry evidence, and matched to a record of real execution. The strongest cases do not simply say the petitioner works in a high-demand field. They show why the proposed work matters to the United States and why the petitioner is specifically positioned to advance it.

Pursuing an EB-2 NIW in financial technology, enterprise architecture, cybersecurity, banking infrastructure, or digital transformation?

Free assessment: immignis.us/contact-us