EB-2 NIW Housing Finance senior executive with 22 years experience in audit, banking, capital markets, and MBS/sukuk supporting U.S. housing-finance modernization.

A senior finance executive with an M.Sc. in Accounting, FCA (Fellow Chartered Management Accountant), CPA, and CGMA certification, bringing over 22 years of experience across Big Four audit, banking, investment finance, capital markets, and housing-finance leadership, was approved for an EB-2 National Interest Waiver as a self-petitioner.

Pakistan national, Saudi Arabia–based, he served as Deputy CFO at a sovereign wealth fund–owned housing finance institution operating in a model broadly comparable to Fannie Mae and Freddie Mac, acquiring mortgage loans, structuring mortgage-backed securities and sukuk, and enhancing liquidity in the residential mortgage market. In this role, he supported over $5 billion in sukuk and debt issuances, $3 billion in facility lines, investor roadshows, capital planning, SAMA regulatory compliance, and mortgage product development.

His proposed endeavor is to provide independent C-level housing finance advisory services in the United States, focused on secondary mortgage market liquidity, alternative credit assessment models, fintech-driven mortgage platforms, green housing finance instruments, community land trust structures, and improved affordable housing access. Approved under Matter of Dhanasar based on extensive cross-market financial leadership and policy-relevant housing finance experience.

The petitioner’s name, employer names, award links, and personal identifiers have been withheld for privacy. Career record, credentials, award history, and outcome are real.

Why this case matters

Housing finance is usually invisible until it fails. A family may think the mortgage decision begins and ends at a local bank, but the ability of that bank to keep making new loans depends on the secondary market behind it. When lenders can sell mortgage loans into a well-functioning secondary market, capital is recycled into new lending. When that market tightens, affordability suffers, credit standards harden, and first-time buyers are pushed further away from ownership.

The United States built one of the world’s most influential housing-finance systems through government-sponsored enterprise activity, mortgage-backed securities, and federal credit support. That system remains enormous, complex, and nationally important. It also faces persistent pressure: affordability constraints, high borrowing costs, limited housing supply, uneven access to mortgage credit, and the need to modernize underwriting and transaction systems.

This petitioner’s background stood out because he was not proposing to enter housing finance from the outside. He had worked inside a foreign secondary mortgage-market institution created to provide liquidity to residential housing finance, using instruments and regulatory relationships that parallel the U.S. model in structure even though the legal and market context is different.

A career built inside financial infrastructure

His career began in audit and accounting and then moved into banking, finance transformation, and executive financial leadership. Over more than two decades, he worked through the mechanics that make regulated financial institutions function: IFRS reporting, central-bank compliance, capital planning, treasury operations, core banking systems, sukuk issuance, investor documentation, and executive decision support. EB-2 NIW housing finance

At one major financial institution, he helped move monthly financial reporting from a slow calendar-based cycle toward real-time access. At another, he implemented IFRS 9 expected credit-loss models, replaced manual Islamic finance processes with digital brokerage workflows, and managed virtual data-room processes for strategic investment activity. He later worked on a $750 million sukuk issuance and received regional recognition through MENA CFO awards, including Emerging CFO of the Year in 2018. EB-2 NIW housing finance

The most relevant stage of the career came in housing finance. As Deputy CFO of a Saudi institution established to improve mortgage-market liquidity, he worked on sukuk and mortgage-backed securities activity, investor relations, capital management, license compliance, IPO-readiness work, and mortgage product strategy. He also contributed to digital mortgage-distribution infrastructure involving bank applications, fintech channels, and other distribution partners. EB-2 NIW housing finance

The proposed U.S. endeavor

The approved NIW was built around an independent housing-finance advisory endeavor, not a conventional job-search plan. The petitioner proposed to advise U.S. housing-finance stakeholders, lenders, fintech platforms, community development actors, and housing-related institutions on practical tools that can expand access, improve capital flow, and reduce friction in the mortgage process.

The proposed work centered on six connected areas:

- Secondary mortgage-market liquidity: advising on structures that help lenders recycle capital and support continued mortgage origination.

- Alternative credit assessment: incorporating documented rent, utility, banking, and cash-flow behavior where appropriate to help evaluate borrowers who are creditworthy but underserved by traditional scoring models.

- Fintech mortgage platforms: improving digital origination, borrower-document collection, underwriting workflow, and servicing coordination.

- Green housing-finance instruments: supporting structures that connect energy-efficiency improvements with financing incentives and capital-market participation.

- Community land trust and affordable-housing finance models: aligning capital tools with long-term affordability frameworks.

- Blockchain-supported property records and title workflows: exploring secure, auditable transaction records to reduce fraud and lower administrative friction where legally appropriate.

The petition did not present these as abstract policy ideas. It linked them to the petitioner’s experience managing large debt issuances, working with mortgage-backed instruments, supporting digital mortgage distribution, and operating inside the finance function of a secondary mortgage-market institution.

EB-2 NIW housing finance: National importance of housing finance as a U.S. economic issue

The national-importance case was grounded in the scale and vulnerability of the U.S. housing-finance system. The U.S. Government Accountability Office has reported that the federal government directly or indirectly backs trillions of dollars in single-family mortgages, including exposure tied to the conservatorships of Fannie Mae and Freddie Mac. EB-2 NIW housing finance That scale makes housing finance a national economic issue, not only a private lending concern.

The affordability context also supported the petition. Recent housing research continues to describe a difficult environment for homebuyers and renters, with high prices, elevated borrowing costs, and cost burdens affecting access to stable housing. EB-2 NIW housing finance Housing policy in 2025 and 2026 has continued to focus on supply, affordability, regulatory burden, manufactured housing, and reducing costs for households.

The petitioner’s proposed work addressed the finance side of that problem: not construction, zoning, or housing production alone, but the capital-market, underwriting, and transaction infrastructure that determines whether housing demand can become sustainable financing. EB-2 NIW housing finance

How the petition was built

The First Prong emphasized both substantial merit and national importance. Housing affordability, mortgage liquidity, underwriting access, and capital-market stability were presented through government and institutional sources rather than unsupported commentary.

The Second Prong was the strongest part of the case. The petitioner’s record included more than 22 years of progressive finance leadership, Big Four audit exposure, senior banking and finance roles, IFRS implementation, capital-market transactions, two regional CFO recognitions, $5 billion-plus in sukuk and debt issuance work, $3 billion in facility lines, and direct executive work inside a secondary mortgage-market institution.

The Third Prong argued that the proposed work required independence. A single employer role would limit the petitioner to one lender, one institution, or one product line. The NIW allowed him to advise across the housing-finance ecosystem, including lenders, fintech platforms, affordable-housing stakeholders, and community-development structures where the public benefit depends on cross-institutional adoption.

The outcome

Approved.

USCIS approved the self-petitioned EB-2 NIW for a senior housing-finance executive whose work connected capital markets, mortgage liquidity, digital finance, and affordable-housing access. The approval recognized that his proposed U.S. work had substantial merit and national importance, that his career positioned him to advance it, and that waiving the job-offer and labor-certification requirements would benefit the United States.

This was not a general finance case. It was a housing-finance case built on a rare institutional analogy: a petitioner who had worked inside a foreign secondary mortgage-market organization and proposed to apply that experience to the U.S. housing affordability and mortgage-access challenge.

For finance executives and housing-finance professionals

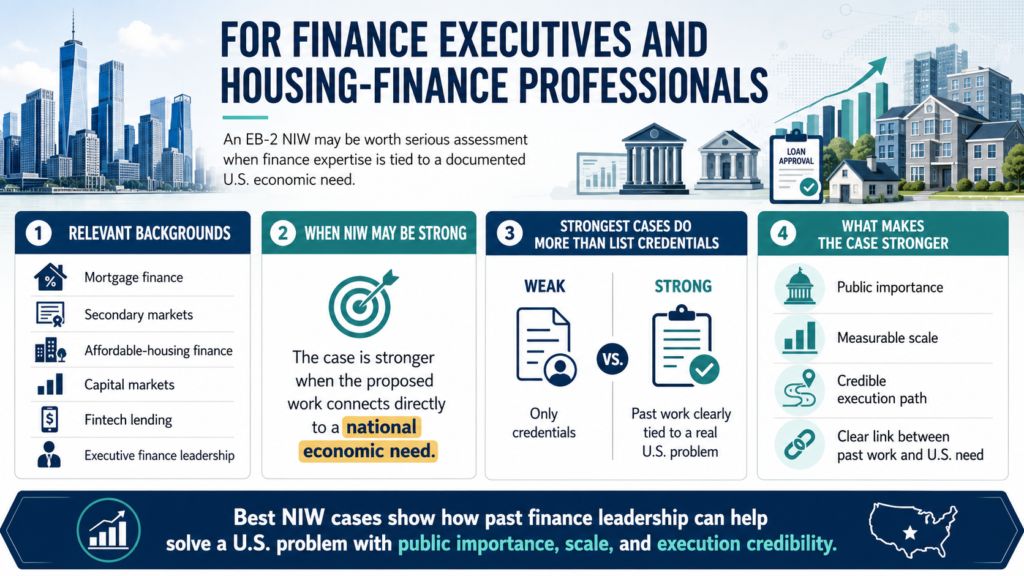

If your background is in mortgage finance, secondary markets, affordable-housing finance, capital markets, fintech lending, or executive finance leadership, the EB-2 NIW may be worth serious assessment when your proposed work connects to a national economic need. The strongest cases usually do more than list credentials. They show how the applicant’s past work maps directly onto a U.S. problem with public importance, measurable scale, and a credible execution path.

Questions housing-finance professionals ask us

Can a finance executive qualify for EB-2 NIW?

Yes. The NIW standard is field-neutral. A finance executive can qualify when the proposed endeavor has national importance and the petitioner is well-positioned to advance it. Housing finance, mortgage liquidity, affordable-housing access, and secondary-market stability can support national importance when the petition connects the work to documented U.S. economic and housing needs.

Why did the secondary mortgage-market experience matter?

It gave the case a direct institutional foundation. Many finance professionals can discuss housing affordability, but far fewer have worked inside an organization created to create mortgage-market liquidity through loan acquisition, securitization, investor activity, and regulatory coordination. That experience made the proposed U.S. advisory work more credible.

Does the case depend on calling the Saudi institution “Fannie Mae”?

No. The safer framing is that the institution performed a broadly comparable secondary-market function. The story can explain the analogy without overstating that the two systems are identical. That distinction keeps the narrative strong and accurate.

What should similar applicants avoid?

They should avoid unsupported academic citations, generic policy claims, and broad statements that do not connect to their own record. A housing-finance NIW should rely on verifiable government and institutional sources and should show specific financial transactions, product work, policy relevance, and execution capacity.

Free assessment: immignis.us/contact-us